New 2025 schema for SAF-T eVAT returns

Norway is to update its schema to version 1.3 from 2025 for its version of the OECD’s Standard Audit File for Tax (SAF-T). This includes v1.3 SAF-T Financial.

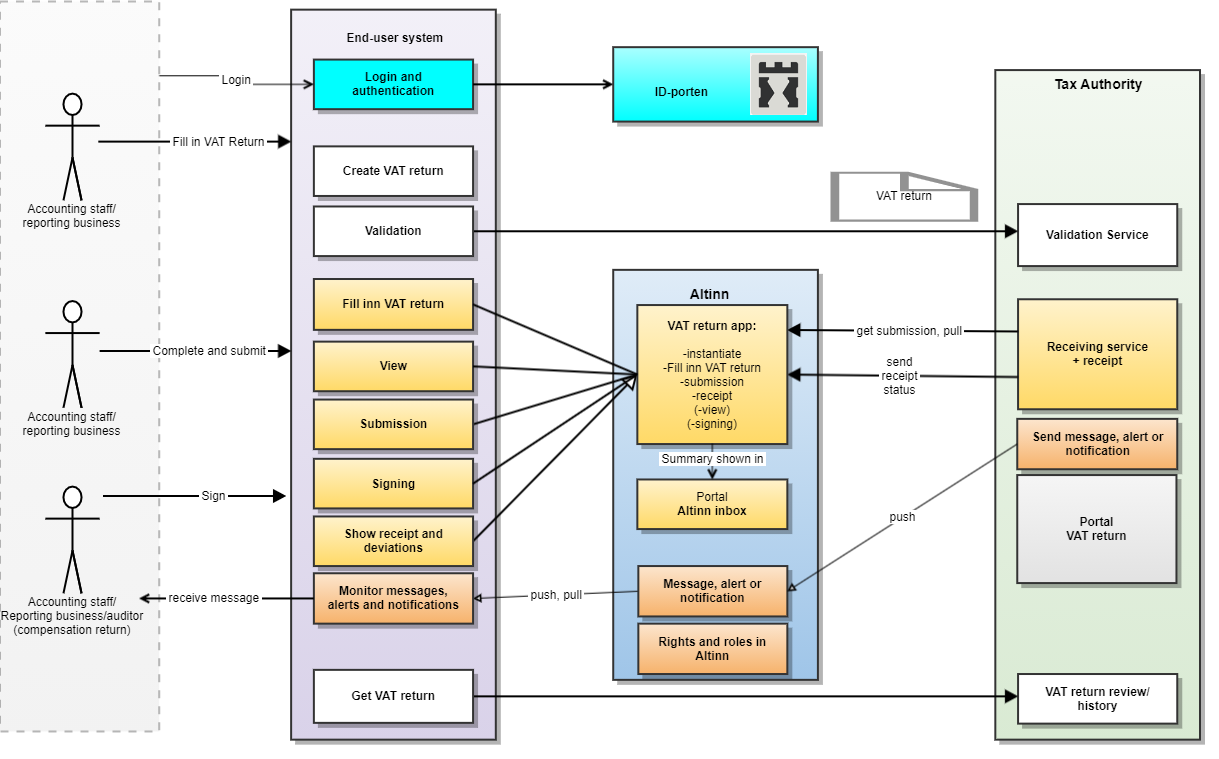

Norway replaced its bi-monthly Value Added Tax return with SAF-T on 1 January 2022. This included an extension of the existing 19 box reporting to 30 boxes to capture all the additional information that is currently captured in the return. Filings will be timed as with the current return schedule – monthly, bi-monthly or annually. This is through the ID-porten online portal, in Norwegian or English languages.

The new VAT-return since 1 January 2022 re-uses the Standard Tax Codes from the SAF-T standard. (Note: the new VAT-return must not be confused with the Norweigan SAF-T Financial file. Only the codes will be re-used – The VAT-return will still be at a very aggregated level).

New RF-0002 and RF-0004 submissions

The following returns were replaced by SAF-T

- Standard return, RF-0002

- Agriculture sector return – RF – 0004

The VAT returns for non-residents completing VAT on Electronic Services (VOES) or VAT on E-Commerce (VOEC) registration are unaffected. Note, there is no change to the existing SAF-T mandate.

Dual Norwegian SAF-T file

Norway introduced mandatory SAF-T filings in 2020 for resident business filing bi-monthly VAT returns. The SAF-T code setup consists of 30 codes, of which 25 will be mandatory in the digital VAT return, provided there is transaction activity related to the specific codes. There are currently two parts to the Norwegian version of SAF-T:

- Financial: General Ledger; Customer master data; Supplier master data; Tax master data. This is supported by stock movements, product data and asset register.

- Cash Register: Locations; Cash register, Cash transactions

API or “Mine MVA-Meldinger” data filing

Norweigan data transmitted via Altinn portal is the main method for sending in SAF-T files. This includes either:

- an API link to ERP’s. Standard SAF-T VAT codes will be used for completing the new VAT return; or

- Via a new portal, Mine MVA-Meldinger”. VAT Groups are recommended to use this path.

These codes were developed during the implementation of SAF-T accounting in 1 January 2020.

The switch to replacing the VAT return requires introduction of transaction level reporting for all sales and purchasing, with proposals for these changes already submitted. It is possible that additional data relating to bad debts, adjustments or input VAT reversals and withdrawals (self-supplies) will also soon be requested.

Note: Norway has indicated that it may accept XML uploads instead of insisting on direct API-based submissions from ERP or accounting statements. Other formats include: pdf, open office xml, open document format, JPG, and PNG.

Live validation of VAT data

It is likely that there will be some basic data checks. This could include VAT validation checks. Invalide entries, ugyldig skattemelding, will be immediately correction before the submission is accepted.

Poland SAF-T replaced its VAT return in October 2020. Check which other countries have implemented SAF-T. If you need to complete any country returns, our VAT Filercan accurately populate any country submission with verified VAT or GST data from our VAT Calculator or VAT Auditor services.

Transactional-level VAT data to come 2024

Note: this will not provide the tax authorities with detailed transactional data. Although the Norwegian authorities will be pursuing this from 2024. This will include:

- VAT numbers of both parties

- Invoice number and date

- Amount

- VAT liability

The digital VAT return is a report on turnover, input and output VAT on an ongoing basis. The taxpayers are not required to submit a full SAF-T file for each VAT period. The ongoing VAT reporting will, however, be based on the standard SAF-T VAT codes and will include aggregated sums of transactions registered on each of these codes. It is therefore important to reconcile the VAT return and SAF-T financial data before submitting the report.

SAF-T promotes easy data exchange

Norway introduced mandatory on-demand SAF-T in January 2020. Prior to that, it had been on a voluntary basis since 2017. Per the Norwegian tax office, the objectives of SAF-T are:

- Serve as an export format for accounting data after request from the Norwegian Tax Administration, public accountants and other parties.

- Serve as archiving format for the necessary accounting data for those who are obliged to keep accounts as stated in the Norwegian bookkeeping legislation.

- Serve as a format for moving data when changing accounting software.

- Serve as a format for moving data from accounting software to other financial systems such as year-end closing systems, tax computation systems, business intelligence software, advisory systems etc.

EU Continuous Transaction Control (CTC) reporting by 2024?

EU VAT in the Digital Age reforms include a channel for harmonised Digital Reporting Requirements (DRR) and Continuous Transaction Controls (CTC) by EU states. This grew from the 2020 EU Tax Action Plan proposals for a fairer and more efficient EU tax regime.

Standard Audit File for Tax SAF-T countries

| Country (click for details) | Date | Scope | |

| 13 | Bulgaria | 2026 | Phased introduction over two years |

| 12 | Ukraine | Jan 2025 | Phased 2025 to 2027 implementation |

| 11 | Denmark | Jan 2024 | Phased implementation from 2024 |

| 10 | Romania | Jan 2022 | Mandatory monthly filings initially large taxpayers (due Jan 2023) |

| 9 | EU OSS & IOSS | Jul 2021 | On-demand for sellers, marketplaces or Intermediaries |

| 8 | Norway | 2020 | Replaced VAT return 2022 |

| 7 | Angola | 2019 | On-demand |

| 6 | Lithuania | 2019 | On-demand; residents and non-residents above €30,000 sales threshold |

| 5 | Poland | 2016 | Mandatory, monthly replaced VAT return Oct 2020 |

| 4 | France | 2014 | On-demand |

| 3 | Luxembourg | 2011 | On-demand |

| 2 | Austria | 2009 | On-demand |

| 1 | Portugal | 2009 | Monthly for residents and non-residents (Jun 2022) |